Learn about the different accounting records you must maintain under GST

Under the GST regime, multiple tax levies have been replaced by a single GST tax. This has led to major changes in the accounts the business owners must maintain. Previously, you would have maintained individual accounts for VAT, excise, CST and other service taxes with separate input, output, and credit entries for each. Now, the new tax regime means a completely new list of accounts, featuring the components of GST.

Every business owner registered under GST must maintain the following records:

Every business owner should maintain the following accounts:

Note: In addition to this, the Commissioner of GST has the authority to apprise business owners to maintain additional accounts/documents for a specific reason or to maintain the accounts in a prescribed manner.

The biggest change GST brings to the table is the concept of Input Tax Credit. The tax you pay on purchasing your inputs (goods or services used for furthering your business) can be used to offset the tax you will pay on your outputs (finished products or services). Another change is GST’s dual-component structure. The tax for intrastate transactions is divided into CGST (Central GST) that must be paid to the Center and SGST (State GST) that must be paid to the State. If it’s an interstate transaction, a single integrated tax called IGST (Integrated GST) has to be paid to the Center. Because of these regulations, the following accounts must be maintained by a registered business owner:

GST also introduces a concept called the electronic ledgers. Once you register for GST in the Government portal, you will get access to 3 types of electronic ledgers:

Let’s now consider a sample transaction and observe how the entries need to be made in the taxpayer’s different accounts.

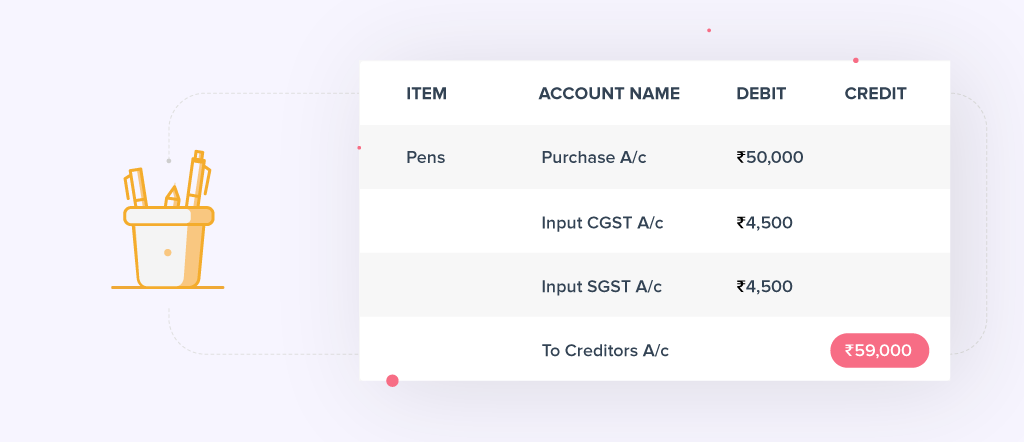

Let’s say Raj purchased pens worth Rs. 50,000 from a GST-registered dealer within his state. The tax applicable to his purchase is 18%, which is broken down into CGST (9%) and SGST (9%). Thus, he pays a total tax of Rs. 9,000 (18% of Rs. 50,000) which is split equally between CGST (Rs. 4,500) and SGST (Rs. 4,500). He can later claim this amount as input tax credit when he has to offset his output tax liabilities.

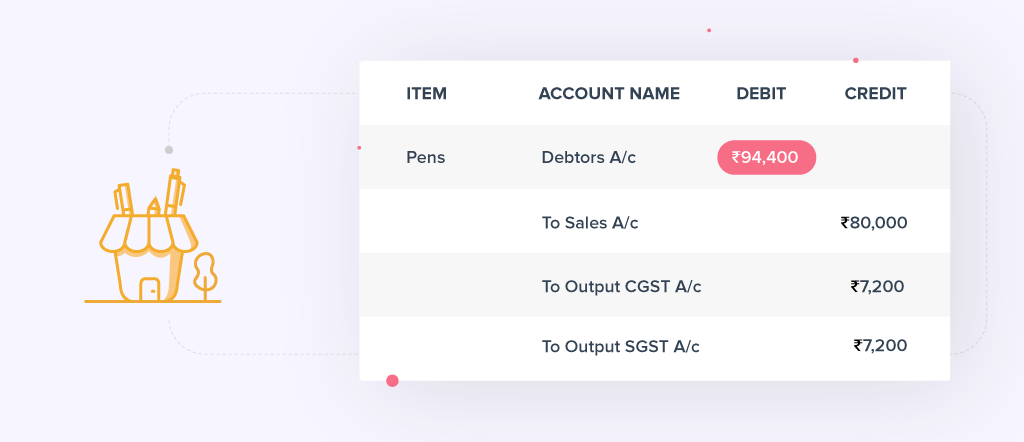

He now sells the pens to another GST-registered dealer for Rs. 80,000. His output tax liability will be 18% of Rs. 80,000, for a total of Rs. 14,400 that is split up equally between output CGST and output SGST.

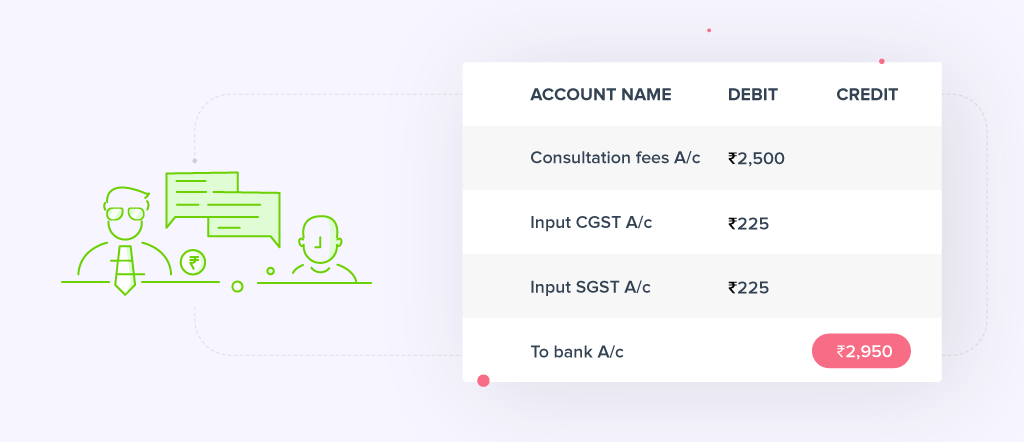

Let’s assume he paid a legal consultation fee of Rs. 2,500 to his CA by cheque. The tax he pays on this will include CGST of Rs. 225 (9% of 2,500) and SGST of Rs. 225 (9% of 2,500).

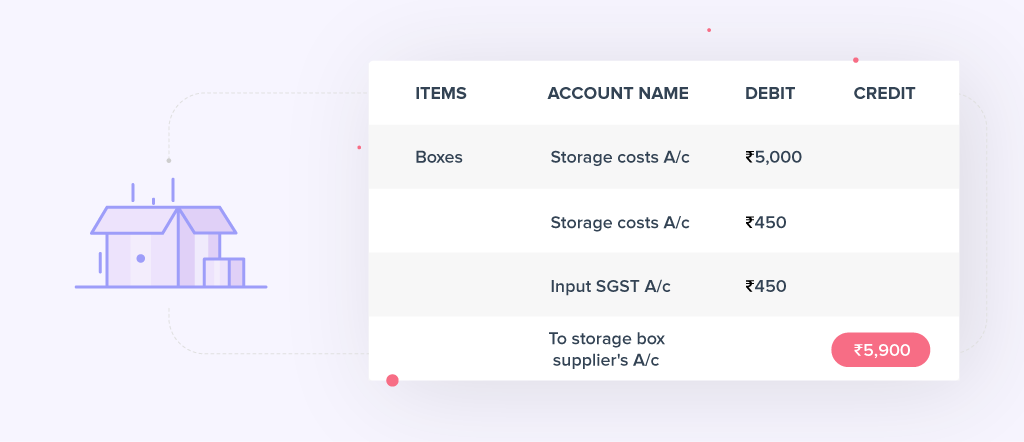

He also paid Rs. 5,000 to purchase the boxes and other materials used for storing the pens. The same tax rates apply here, so he pays CGST of Rs. 450 (9% of 5,000) and SGST of Rs. 450 (9% of 5,000).

Raj’s total tax liability

Let’s now observe how Raj’s total tax payable is calculated.

Total tax payable = 2,025 + 2,025 = 4,050

If Raj has any ITC left after paying his tax obligations, it will be carried over to the next year.

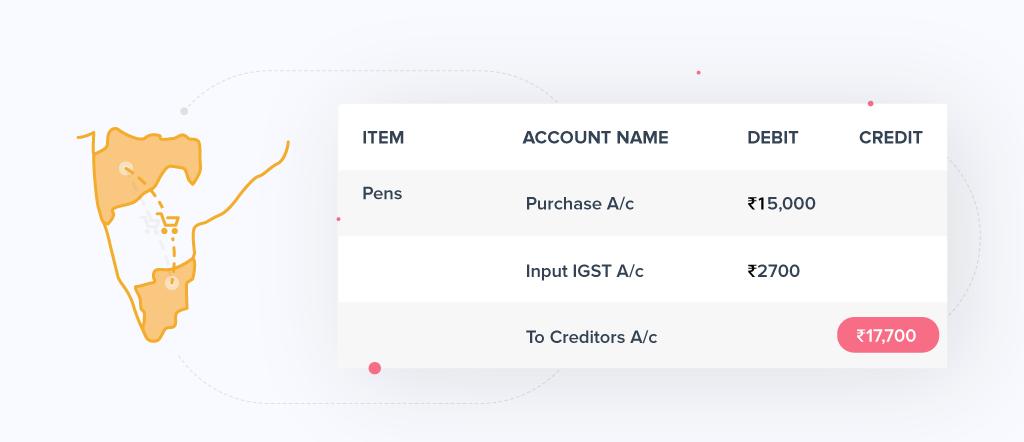

Let’s say Raj purchased pens worth Rs. 15,000 from a GST-registered dealer from outside his state. The tax rate on his purchase is 18%. Thus, he pays an IGST of Rs. 2,700 (18% of 15,000), which he can later avail as input credit.

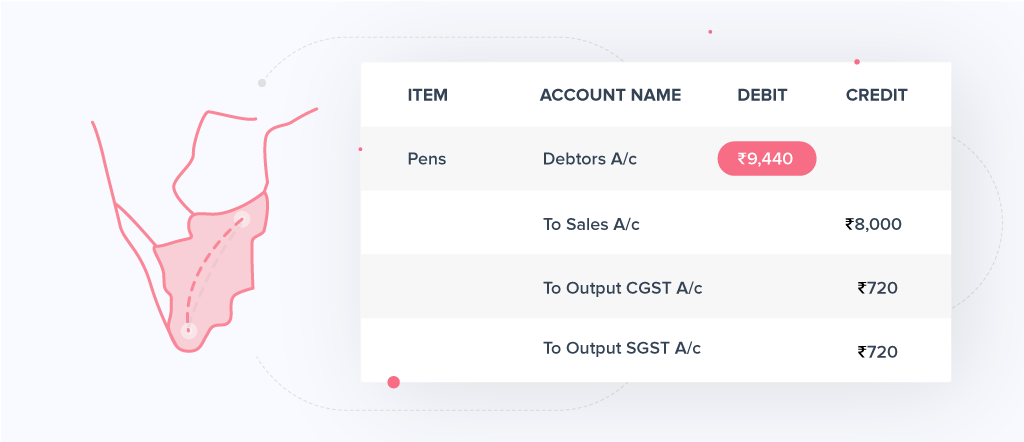

He now sells some of his pens locally for Rs. 8,000. His output tax liability will be 18% of Rs. 8,000, for a total of Rs.1,440 that is split up equally between output CGST and output SGST.

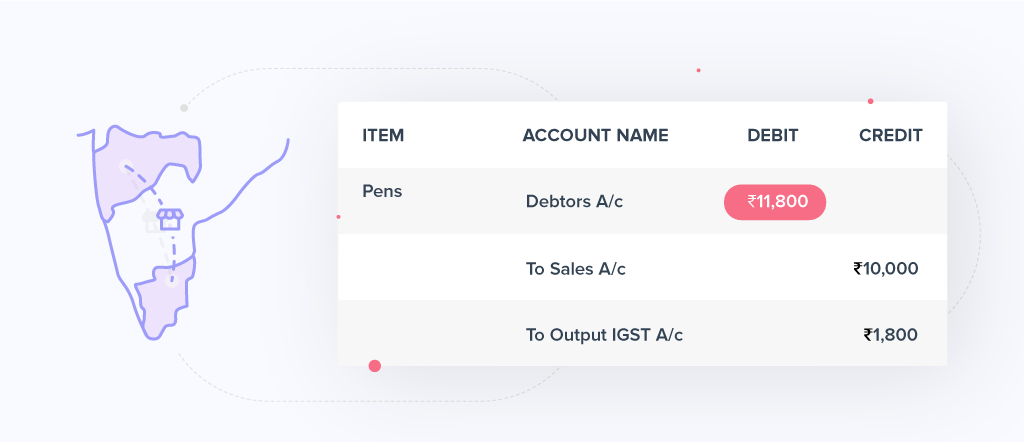

He sells his remaining pens outside his state for Rs.10,000. The output tax liability for these will be an IGST of 18% of Rs. 10,000, which equals Rs. 1,800.

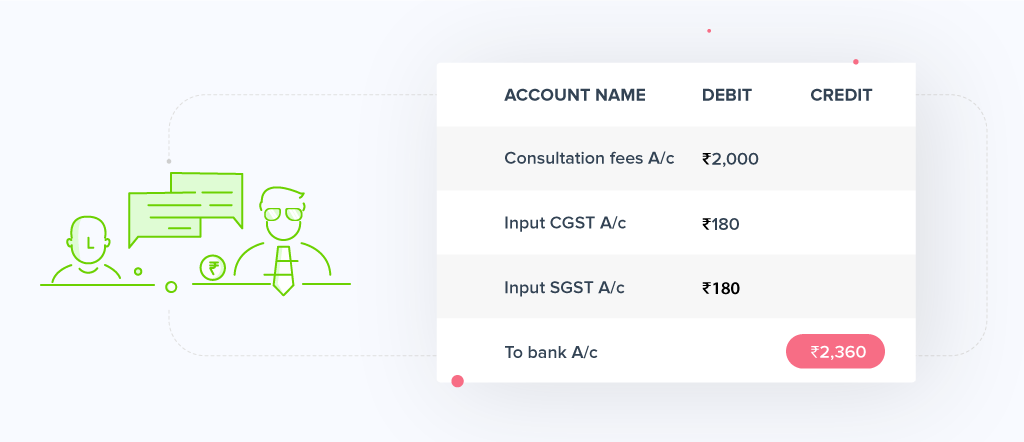

Let’s assume he paid a legal consultation fee of Rs. 2,000 locally to his CA by cheque. The tax he pays on this will include CGST of Rs. 180 (9% of 2,000) and SGST of Rs. 180 (9% of 2,000).

Raj’s total tax liability

Remaining tax payable = 540 – 360 = 180

The GST law dictates that every registered taxable person must maintain their book of accounts for a period of at least 6 years from the last date of filing of the relevant annual return. These records and documents should be maintained at all the related business locations as mentioned in the registration certificate.

© 2022 GSTNREGISTRATION.COM

Powered by: Prologic Web Solutions Pvt Ltd